Global

Global Singapore

Singapore United States

United States Hongkong

Hongkong Group

Group.jpg)

US Macro Strategy Weekly Report

James Ooi/ uSMART Market Strategist

Over 13 years of experience in buy-side and sell-side of capital markets

Former Fund Manager of renowned asset management firm

Focus on fundamental analysis and macro-outlook for US & Singapore markets

SGX Academy trainer

This Week’s Market Outlook

- This week, significant economic data and events in the United States includes the release of the New Home Sales on Tuesday, GDP data on Thursday, May PCE inflation data on Friday. Additionally, Powell will be speaking at a European Central Bank forum on central banking on Wednesday.

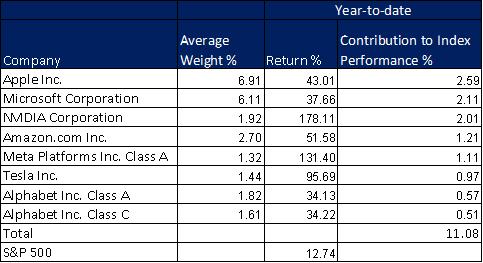

- 7 big tech stocks accounted for nearly 87% of the year-to-date gains of the S&P 500, suggesting that the market rally lacks breadth (Figure 1).

Figure 1: These 7 Tech Stocks Command Almost 87% Of The S&P 500’s Gains.

Source:uSMART, Bloomberg, 26 June 2023

- The NYSE FANG+ Index has reached its target price based on the inverted head and shoulders pattern, and it is currently experiencing profit-taking activities (Figure 2). This suggests that US stocks might undergo corrections, as traders may lack bullish signals to continue driving up stock prices of big tech names.

Figure 2: NYSE FANG+ Index

Source: uSMART, Tradingview, 26 June 2023

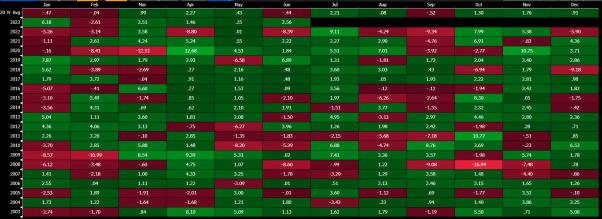

- The S&P 500 has recorded a year-to-date increase of 12.74% (Figure 3), primarily driven by the strong performance of tech-related stocks. However, in June, we are starting to witness a broader market rally across different sectors. Nevertheless, AI optimism seems largely priced in and AI trade seems too crowded at the moment. Tech-related sectors may only have limited upside potential, and a correction seems long

Figure 3: Monthly performance of the S&P 500

Source: Bloomberg, 26 June 2023

- Looking ahead, the probability of a July correction based on seasonality is not high (Figure 4), as observed over the past 20 years. During this period, the average return in July for the S&P 500 has been 2.21%. Additionally, the probability of experiencing a negative return in July is 25%, as the S&P 500 had negative returns in 5 out of the past 20 years.

Figure 4: Monthly performance of the S&P 500 over the past 20 years.

Source: uSMART, Bloomberg, 26 June 2023

- Core CPI, which excludes volatile food and energy prices, experienced a year-over-year increase of 5.3% in May (Figure 5), down from 6.6% in September 2022. However, the core CPI remains at a level that is considered too high for the Federal Reserve's comfort, reinforcing the narrative of higher rates for a longer period.

Figure 5: U.S. consumer price index (Year-over-year percent change through May 2023)

Source: Bloomberg, 26 June 2023

Conclusion:

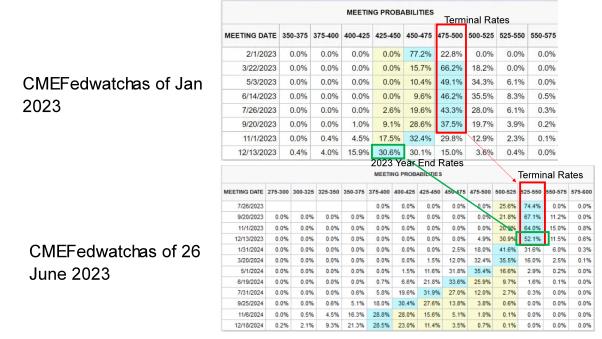

- Investors should pay close attention to news headlines to gauge whether market participants are becoming concerned about the “higher rates for longer” narrative again. The year-to-date equity market rally was partly driven by dovish monetary policy predictions. In early Jan, market participants expected the terminal rates is close, projected to be around 4.75% to 5%, and subsequently reduce rates by 50 basis points in the November and December 2023 FOMC meetings. However, according to the latest CME FedWatch (Figure 6), market expectations have shifted. The current projection is for the FOMC to raise rates by 25 basis points in the July FOMC meeting, resulting in a terminal rate range of 5.25% to 5.5%, with no rate cuts anticipated for the remainder of the year. Despite this renewed narrative of "higher rates for a longer," the equity market has not yet undergone a correction in response. We still think that the risk of steep correction is high.

Figure 6: FOMC Meeting Probabilities

Source: CME Fedwatch, 26 June 2023

- Earnings are not experiencing a collapse, but there is a need to lower forward profit expectations as they are still unrealistically high.

- We maintain our short-term bearish view and mid-to-long-term bullish outlook. Therefore, it is unwise to completely exit the market. We anticipate that big tech names, which have significantly contributed to the year-to-date rally, will likely play a role in the decline of the S&P 500 in near term. However, we also expect an expansion of market breadth, meaning that while big tech may exert downward pressure on the overall market, other stocks could help cushion the market decline.

- Currently, there are several high-quality companies, such as Apple, Amazon, Visa, Tesla, Costco, and Microsoft, that continue to demonstrate strong long-term EPS growth potential. Investors may consider gradually establishing long-term positions in these companies. Additionally, investors can also explore ETFs like SPY, QQQ, and SUSA to capture some market returns.

Follow us

Find us on Twitter, Instagram, YouTube, and TikTok for frequent updates on all things investing.

Have a financial topic you would like to discuss? Head over to the uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimer:

This article is intended for general circulation and educational purpose only and does not take into account of the specific investment objectives, financial situation or particular needs of any particular person. You should seek advice from a financial adviser regarding the suitability of the investment products mentioned. In the event you choose not to seek advice from a financial adviser, you should consider whether the investment product in question is suitable for you.

Past performance figures as well as any projection or forecast used in this article, are not necessarily indicative of future performance of any investment products. Your investment is subject to investment risk, including loss of income and capital invested. The value of the investment products and the income from them may fall or rise. No warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this article. Overseas investments carry additional financial, regulatory and legal risks, you should do the necessary checks and research on the investment beforehand.

The information contained in this article has been obtained from public sources which the uSMART Securities (Singapore) Pte Ltd (“uSMART”) has no reason to believe are unreliable and any research, analysis, forecast, projections, expectations and opinion (collectively “Analysis”) contained in this article are based on such information and are expressions of belief only. uSMART has not verified this information and no representation or warranty, express or implied, is made that such information or Analysis is accurate, complete or verified or should be relied upon as such. Any such information or Analysis contained in this presentation is subject to change, and uSMART, its directors, officers or employees shall not have any responsibility for omission from this article and to maintain the information or Analysis made available or to supply any corrections, updates or releases in connection therewith. uSMART, its directors, officers or employees be liable for any or damages which you may suffer or incur as a result of relying upon anything stated or omitted from this article.

Views, opinions, and/or any strategies described in this article may not be suitable for all investors. Assessments, projections, estimates, opinions, views and strategies are subject to change without notice. This article may contain optimistic statements regarding future events or performance of the market and investment products. You should make your own independent assessment of the relevance, accuracy, and adequacy of the information contained in this article. Any reference to or discussion of investment products in this article is purely for illustrative purposes only, is not intended to constitute legal, tax, or investment advice of any investment products, and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products mentioned. This article does not create any legally binding obligations on uSMART. uSMART, its directors, connected persons, officers or employees may from time to time have an interest in the investment products mentioned in this article.